Eltezam – Self-Service Debt Recovery Platform

Overview

Eltezam is a self-service debt recovery platform designed for Tabby and later expanded to external partners. The goal was to reduce operational costs and improve recovery rates by enabling overdue customers (90+ days) to independently manage and repay their debt. This case study highlights how I led the design of a product tailored for a vulnerable, distrustful user base while achieving measurable business impact.

Business opportunity

When I joined the project, debt collections in Eltezam primarily relied on phone calls from agents. We saw an opportunity to improve efficiency by enabling users to manage and repay their debts independently, without agent involvement. This approach could reduce operational costs and increase recovery rates. From the user’s perspective, it also offered a more convenient way without the need to interact with collection agents.

Users

Our users were people who were over 90 days late on their repayments. From interviews with collection agents, we learned that they:

- Often struggle financially and can’t afford big one-time payments.

- Live in close-knit communities and could ask someone they trusted for help with payments.

- Value flexibility given the tough financial situation.

- Avoid speaking to agents and are very cautious about scams or pressure.

Solution

Together with the team, we defined a vision — Eltezam is a lighthouse in the ocean of credit darkness.

We designed the Eltezam digital portal with a focus on:

- Building trust through clear branding, simple language, and use of personal details like the user’s name and the creditor’s logo in the interface.

- Instant and flexible repayment options that meet users’ needs.

Key features

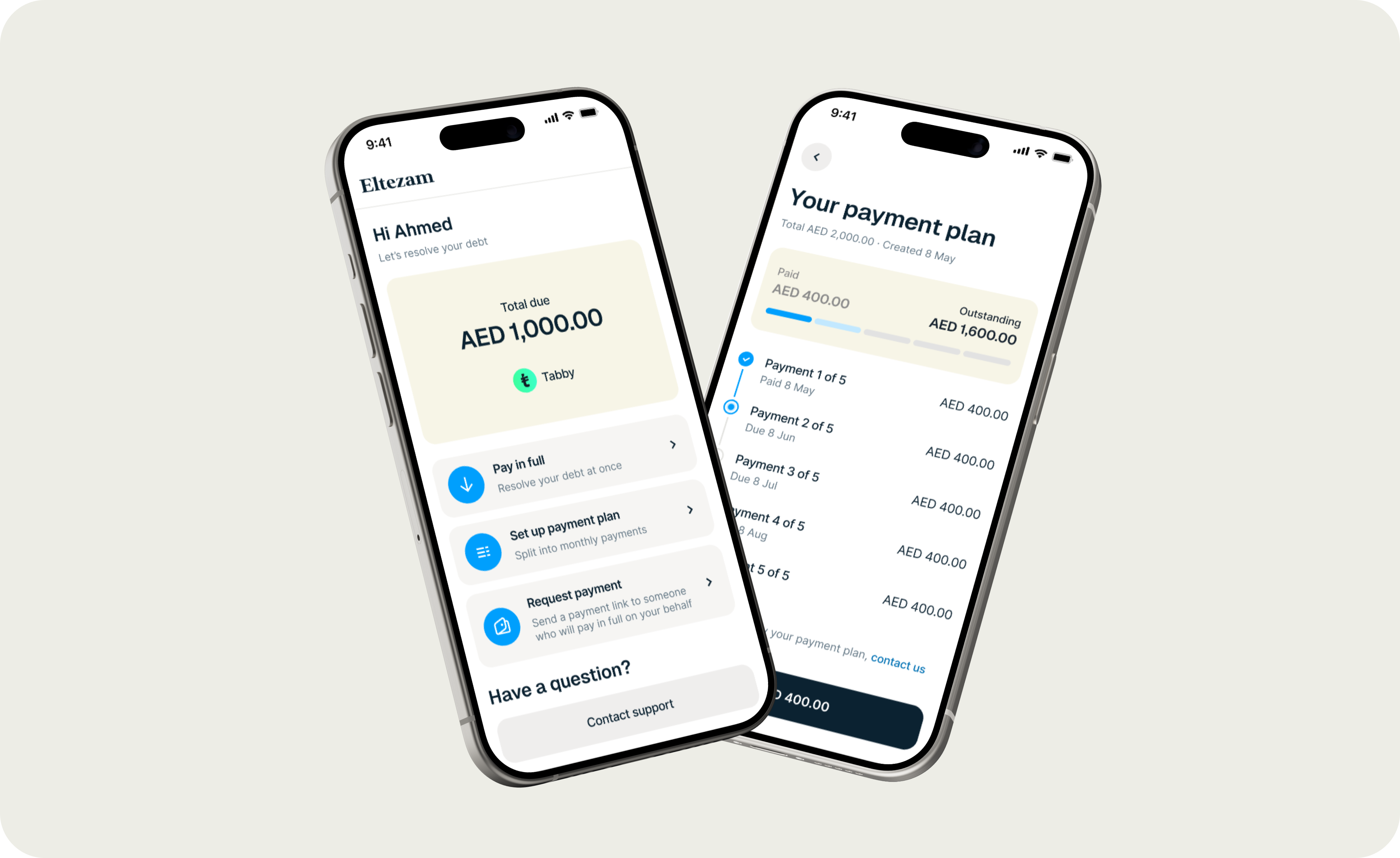

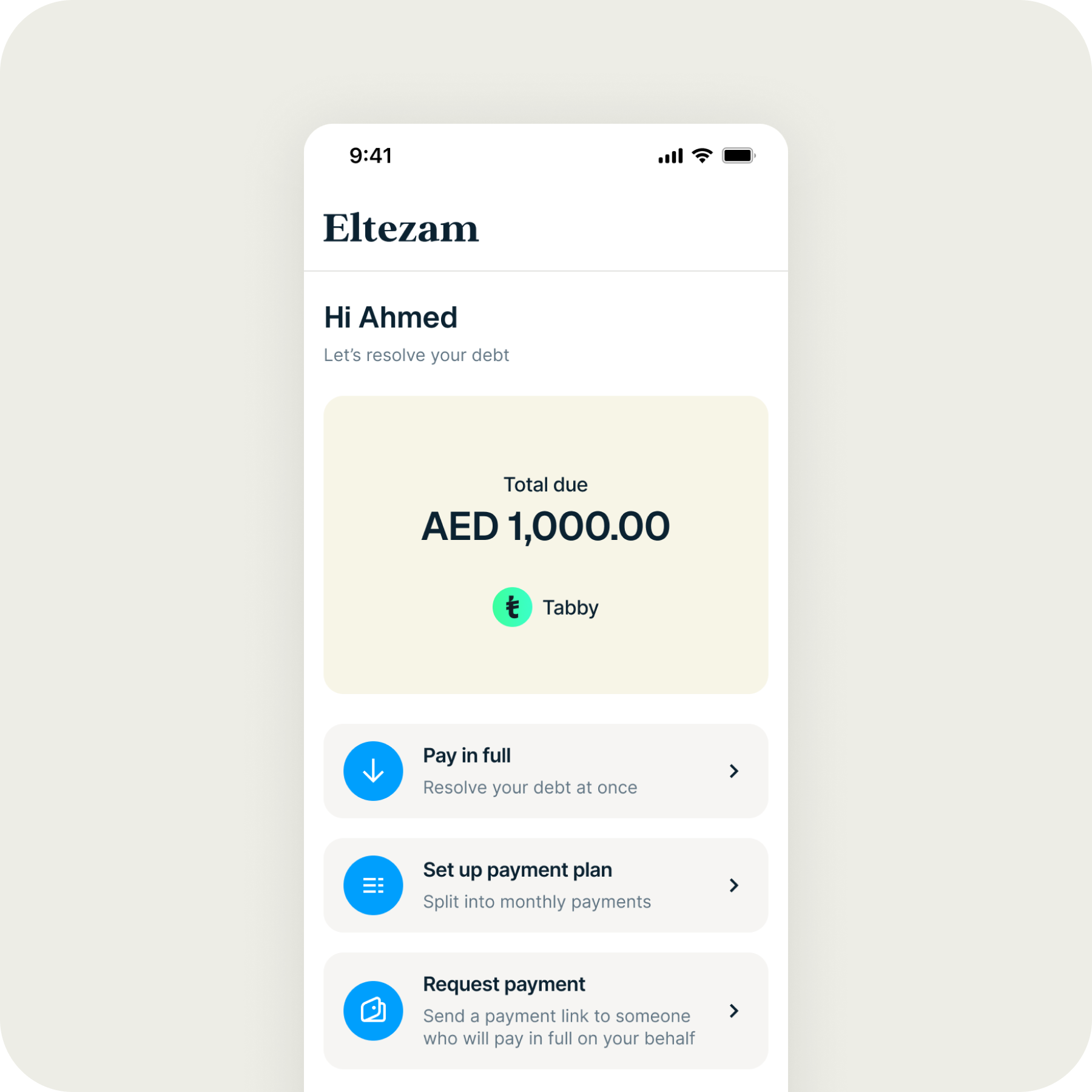

Main page

- Clean, simple layout with three payment options

- Personalised with the user’s first name

- Displays the creditor’s logo and company name

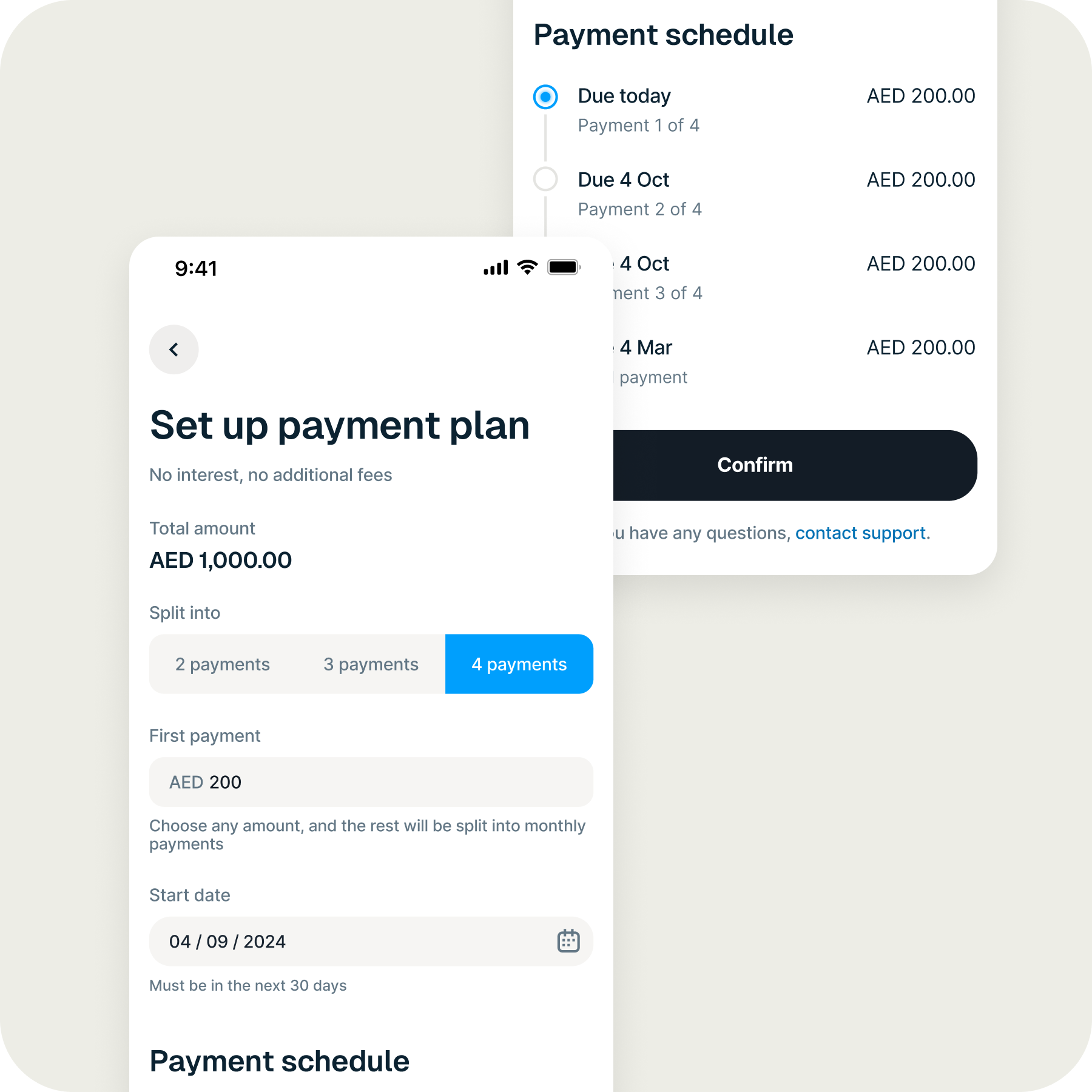

Custom payment plans

Users could choose the number of payments, start date, and first payment amount. We aimed to offer maximum flexibility to fit each user’s financial situation.

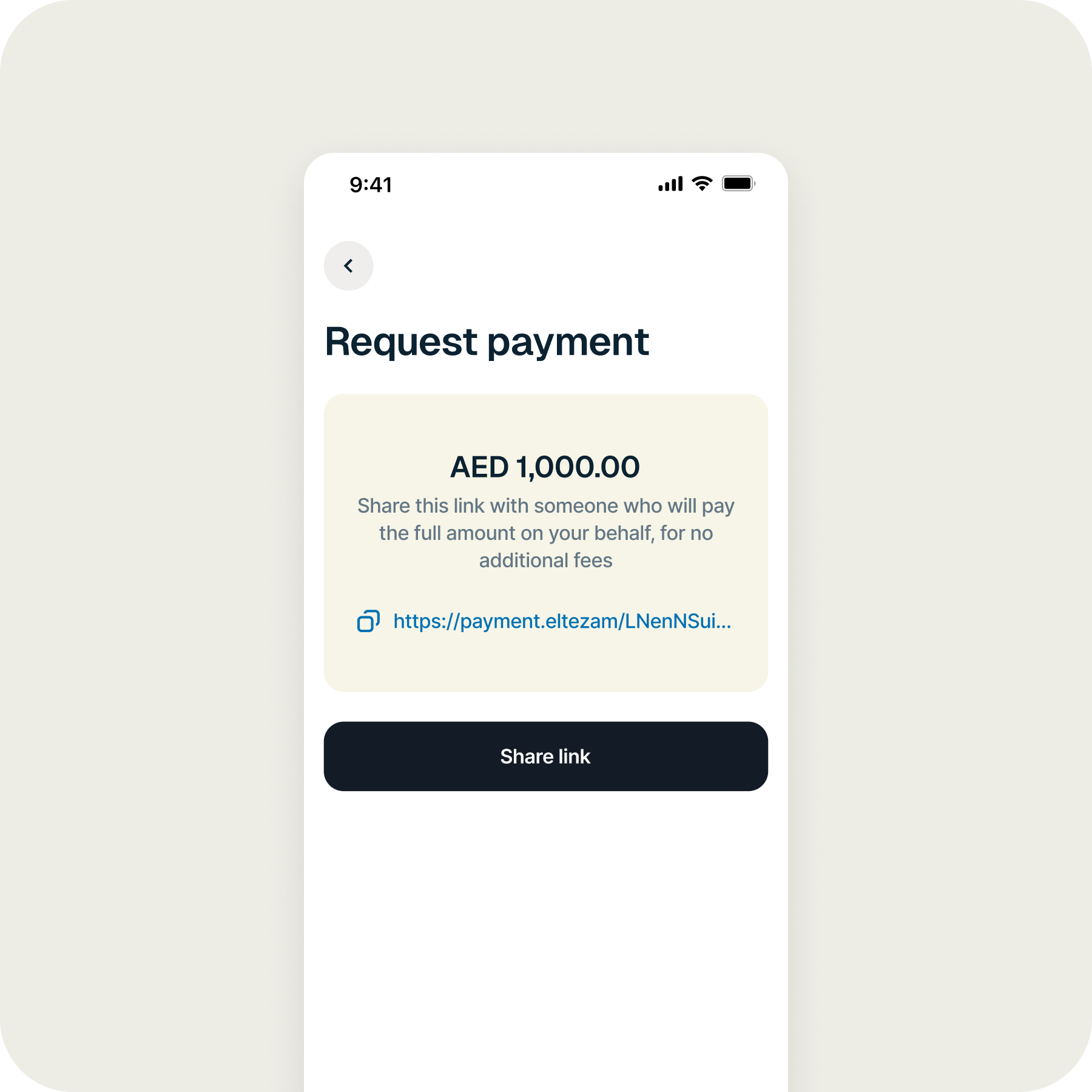

Request payment

Users could ask friends or family for help by sending them a secure payment link.

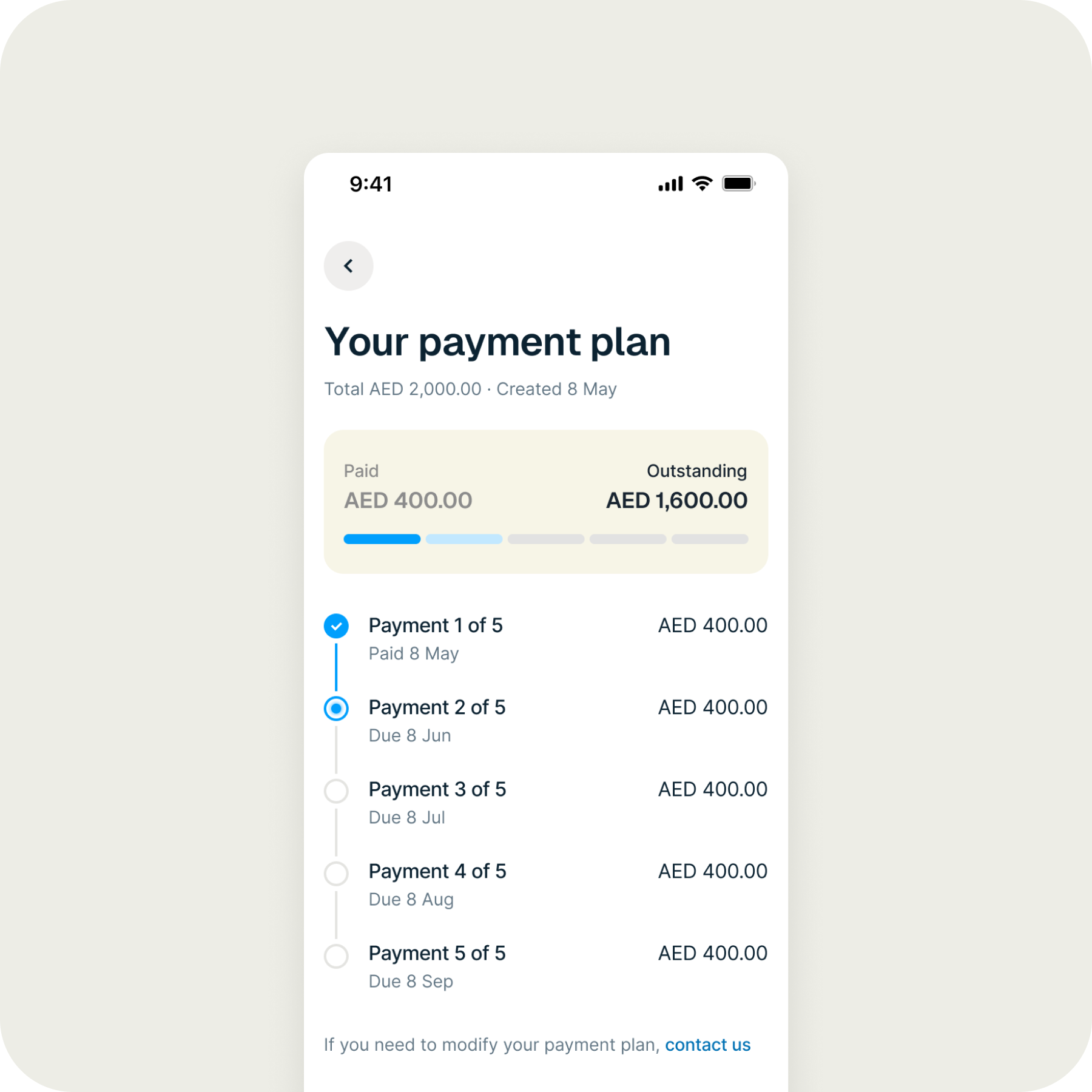

Track payment plan progress and repayments

Once the payment plan was set up, users could track their progress and make repayments through the portal.

Usability test

As this was our first self-service product, we conducted moderated usability tests using mid-fidelity prototypes of the portal.

Key goals

- Validate clarity of the interface

- Ensure users could use key features, especially setting up a payment plan

- Identify concerns and collect ideas for future iterations

We received positive feedback from users:

I hope not ever need to use it. But if I had to, I think it’s a convenient way

It will be very helpful, especially breaking down the payment into smaller payments

The results validated our direction and gave us confidence to proceed with the MVP launch. The test also helped refine the payment plan flow by simplifying terminology and highlighting opportunities for future improvements.

Challenges & iterations on payment plans

When we first launched the payment plans, we tried to make payment plans as flexible as possible to support users going through tough financial times. For example, we allowed very small first payments and let users choose a start date up to a month later. But this approach quickly led to problems:

- Some users abused this flexibility without serious intent to pay

- The maximum of 4 instalments wasn’t enough for people with large debts

- Most importantly, very few users actually made the first payment — only 9.6%

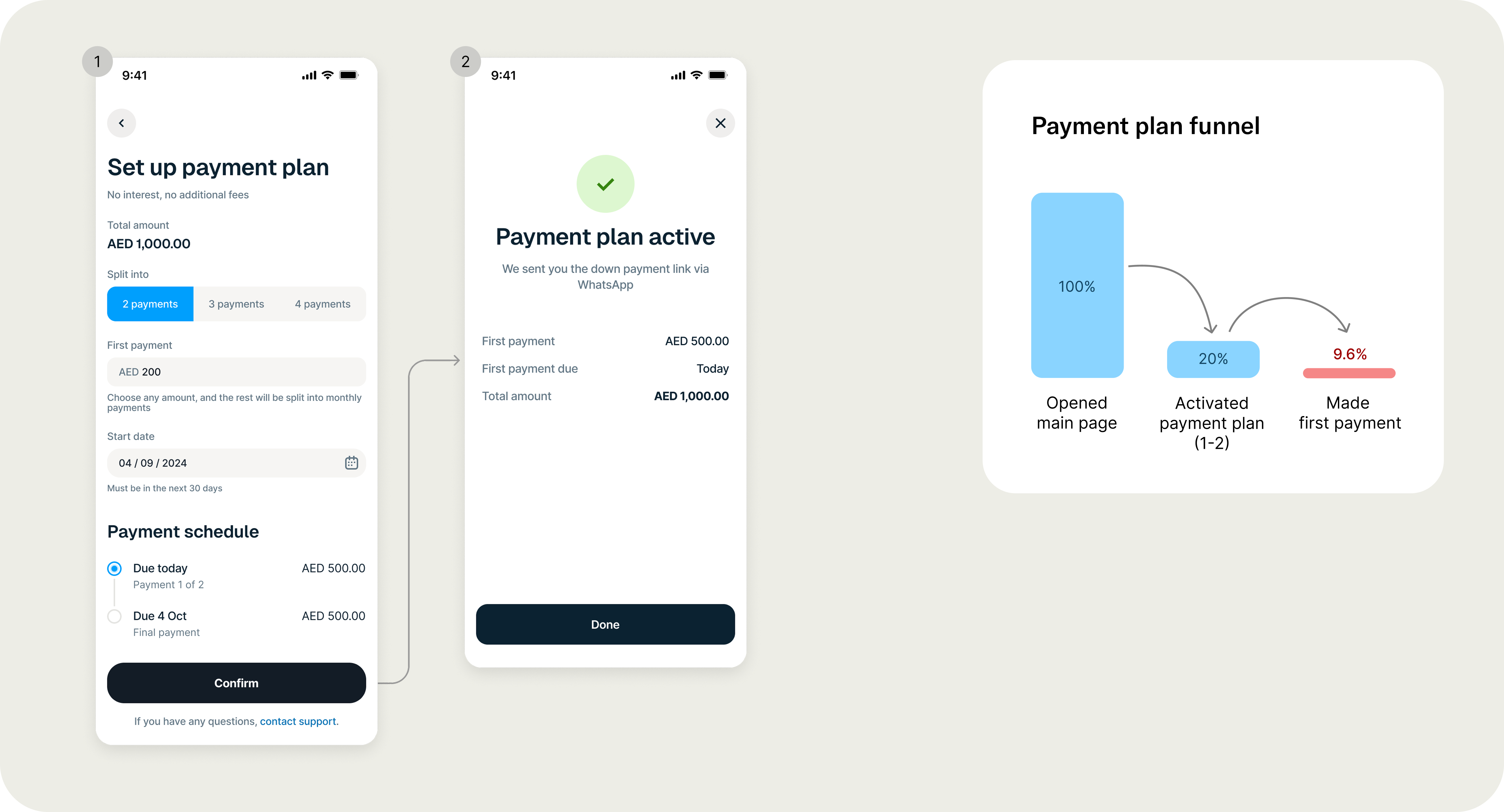

Initial flow

Users could activate a plan in one click, choose a start date up to a month later, and set a very low first payment.

The most obvious solution to improve the low first payment rate was to require it to activate the plan. But that wasn’t ideal from a business point of view. Many users needed some time to find money, and allowing activating the plans gave us the chance to send additional communications, which is a key part of collections. Also, our payment system didn’t yet support all the options users needed. So, we decided to let users activate the plan without paying immediately, but added a strong call-to-action to guide them to pay.

To improve the flow, we spoke to our collections team, people who deal with users daily, and ran a series of experiments:

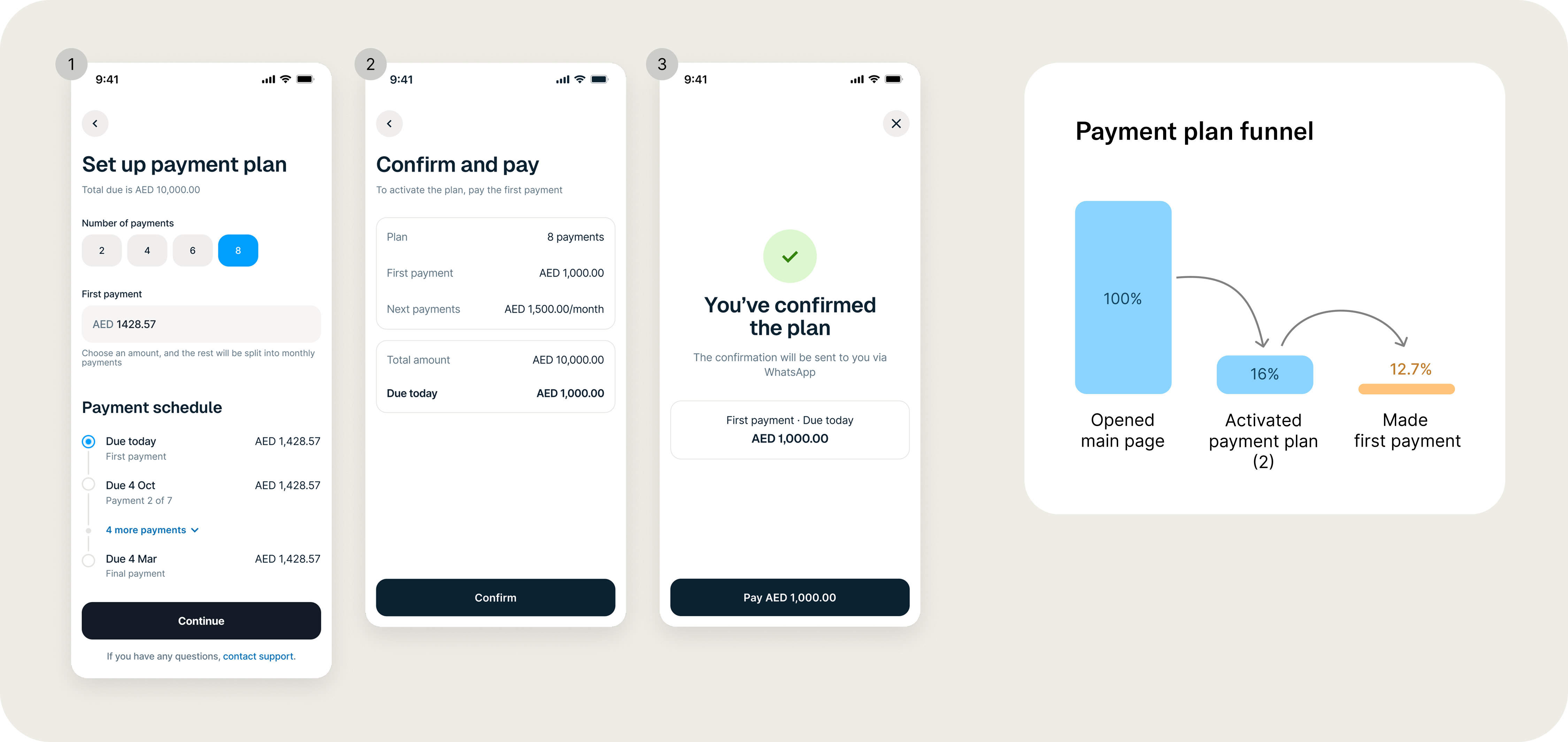

- Restricted flexibility: removed the “start later” option and limited plans to start immediately

- Added a confirmation step to avoid accidental activations

- Allowed more instalments for larger debts

- Kept the option to create a plan without upfront payment, but added a clear CTA to make the first payment

Updated flow

More instalment options for large debts, users confirm the plan before activation, with limited start date options and a CTA to make the first payment.

After these changes, we saw improvements:

- The plan activation rate dropped slightly from 20% to 16%

- But the number of users who made their first payment grew from 9.6% to 12.7%

This showed that small design tweaks and clearer steps helped users commit more and helped the business recover more debt.

Design system

Eltezam needed to look different from Tabby, as it was positioned as a separate, independent service. To achieve that, I collaborated with the developers and created a custom theme based on Tabby’s existing design system. I reused core components but changed the typography and color palette to match Eltezam’s brand. I also added the missing components I needed into Tabby’s shared Storybook, so we could keep things consistent while giving Eltezam its own look and feel.

My contribution

- Led the end-to-end product design, user research, and contributed to shaping the product strategy

- Drove the design from concept to launch, working closely with product and engineering

- Created the visual identity and a custom design system for Eltezam, built on top of Tabby’s design system

Impact

- 68% of Tabby’s customer base used Eltezam in its first year, leading to a significant reduction in collection costs

- 18% of users who landed on the main page activated a payment plan, and successful first payments increased by ≈30%

- Achieved a market-leading total recovery rate

My learnings

This was a unique experience designing for a very specific and vulnerable user group, and I learned a lot throughout the process.

- I saw how important it is to truly empathise with users, especially when they’re in difficult financial situations.

- I learned to design in a way that balances trust and safety — anticipating potential misuse while still supporting users’ needs.

- I worked closely with business developers and the collections team, and I learned that deep cross-functional collaboration is key to building a successful product.